How to Make Safe, Natural Holi Colors at Home?

Jul 04, 2026By Aishwarya Rao

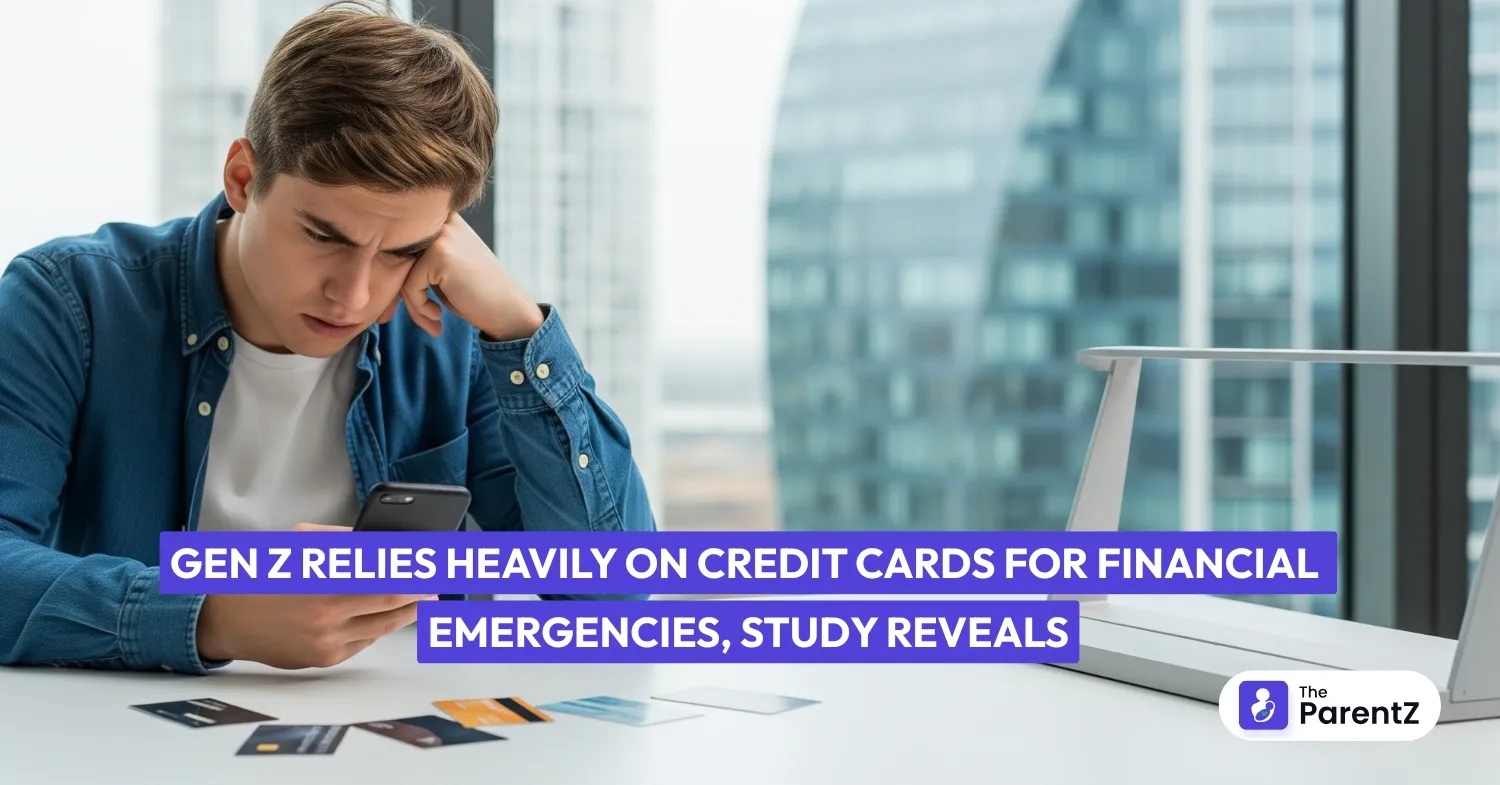

If you're a parent watching your Gen Z child handle their finances, you might feel worried about their approach to money. A recent study by Credit One Bank found something that might alarm you: 62% of Gen Z don't have emergency savings, and many rely heavily on credit cards when unexpected expenses hit.

Before you panic or lecture them about financial responsibility, take a deep breath. This isn't about your child being irresponsible or lazy. There's a much bigger picture here that we need to understand.

Your child is living in a completely different economic world than the one you grew up in.

The cost of everything has skyrocketed. Rent that might have been $800 in your day could easily be $1,800 now. Groceries cost more. Gas costs more. Even a simple coffee costs more. But entry-level salaries haven't kept pace with these increases.

Your Gen Z child has also graduated or is graduating into a job market that looks nothing like the one you did. Many jobs are now considered "gig work," such as Uber, freelance writing, or contract positions. These jobs rarely come with benefits like health insurance or retirement contributions. There's no job security, no clear path up the corporate ladder.

On top of all this, many are carrying student loan debt that can feel crushing. The average student loan debt is now over $30,000, and for many, it's much higher.

When your child uses a credit card for an emergency, they're not being reckless. They're often making the only choice available to them in that moment.

Think about it this way: if your rent is $1,200, your car payment is $300, student loans are $250, and you're making $3,000 a month, there's not much left over for building an emergency fund. When the car breaks down or they need to see a doctor, what choice do they have?

Credit cards become their safety net because they don't have the luxury of building a traditional emergency fund quickly enough.

Here's something interesting that might surprise you: your Gen Z child probably knows more about personal finance than you think. They've grown up with endless information at their fingertips. They watch TikToks about budgeting, follow Instagram accounts about investing, and read Reddit threads about money management.

But here's the problem: having information isn't the same as having experience or confidence to act on it. It's like having a cookbook but never having cooked before. They know what they should do, but they're not sure how to actually do it in their specific situation.

Your Gen Z child has watched previous generations work themselves to exhaustion, sacrifice family time for career advancement, and still struggle to afford homes or secure retirements. They've decided that maybe there's a different way to think about success.

Instead of just focusing on accumulating money, they value experiences, flexibility, and mental health. They want to travel, spend time with friends, and have a work-life balance. This isn't selfish; it's actually healthy. But it can sometimes mean they prioritize immediate experiences over long-term savings.

Remember, your child grew up watching the financial crisis unfold. They saw their parents or their friends' parents lose homes, jobs, and retirement savings. They've witnessed banks foreclosing on families and charging excessive fees. This has made them naturally suspicious of traditional financial institutions.

When a financial advisor tells them to "just save more," it can feel tone-deaf. They think, "Easy for you to say as you didn't graduate into a pandemic with student loans and sky-high rent."

How can you support your child without making them feel judged or misunderstood?

Your Gen Z child isn't financially irresponsible. They're adapting to a challenging economic environment with the tools available to them. Yes, relying on credit cards for emergencies isn't ideal, but understanding why they're doing it is the first step to helping them build better financial habits.

Remember, they're also dealing with challenges you never faced: social media pressure, a gig economy, and political uncertainty. Their approach to money reflects their attempt to handle all of this.

Instead of focusing on what they're doing "wrong," focus on supporting them in building financial skills gradually. Small steps forward are still progress.

The goal isn't to make them manage money exactly like you did. The goal is to help them find a sustainable approach that works for their lives, their values, and their economic reality.

TheParentZ offers expert parenting tips & advice, along with tools for for tracking baby and child growth and development. Know more about Baby Growth and Development Tracker App.It serves as an online community for parents, providing valuable information on baby names, health, nutrition, activities, product reviews, childcare, child development and more

Disclaimer:

The views, thoughts, and opinions expressed in this article/blog are solely those of the author and do not necessarily reflect the views of The ParentZ. Any omissions, errors, or inaccuracies are the responsibility of the author. The ParentZ assumes no liability or responsibility for any content presented. Always consult a qualified professional for specific advice related to parenting, health, or child development.

Conversations (Comments) are opinions of our readers and are subject to our Community Guidelines.

Be the first one to comment on this story.